Chinese High-Net-Worth-Individuals are still spending. Just not where most brands expect.

Drawing on multiple 2025 primary research reports, this article reveals where China's high-net-worth consumers are actually directing their spending, and what that means for the brands trying to reach them.

In 2025, mainland China's personal luxury goods market shrank by 3%–5%. Although the market has readjusted from the sharp 18%–20% decline seen in 2024, pressure remains. At the brand level, LVMH reported an 8% year-on-year decline in Asia-Pacific fashion and leather goods sales in the first half of 2025. Gucci closed 18 stores in mainland China over the same period, marking its sixth consecutive quarter of negative growth. (Source: Bain & Company China Personal Luxury Report, January 2026.) These figures are real, widely reported, and have substantially changed how the industry perceives China's high-net-worth consumer market.

However, there is an important distinction to be made. These figures reflect the aggregate performance of the luxury market, not the specific spending behaviour of China's true high-net-worth individuals (HNWIs). The data sources referenced in this article define HNWIs slightly differently. For example, the YFLife x Hurun report defines HNW households as having net assets of at least RMB 10 million (approximately 2.066 million households). The Hakuhodo x Hurun report’s sample is drawn from households with disposable assets of at least RMB 6 million. Both reflect trends among China's affluent and high-net-worth consumer base, but their samples and definitions of high net worth differ fundamentally. Readers should bear this in mind when comparing figures.

When we focus directly on the HNWI group, the data tells a different story.

60% of Chinese HNWIs report their desire to spend as "increased or unchanged" — higher than the middle-class figure of 57%. (Source: Hakuhodo x Hurun, compared with pre-pandemic levels)

Consumers haven’t lost their appetite to spend. The real shift is where spending now flows. For brands and destinations hoping to reach Chinese HNWIs, understanding that shift is crucial.

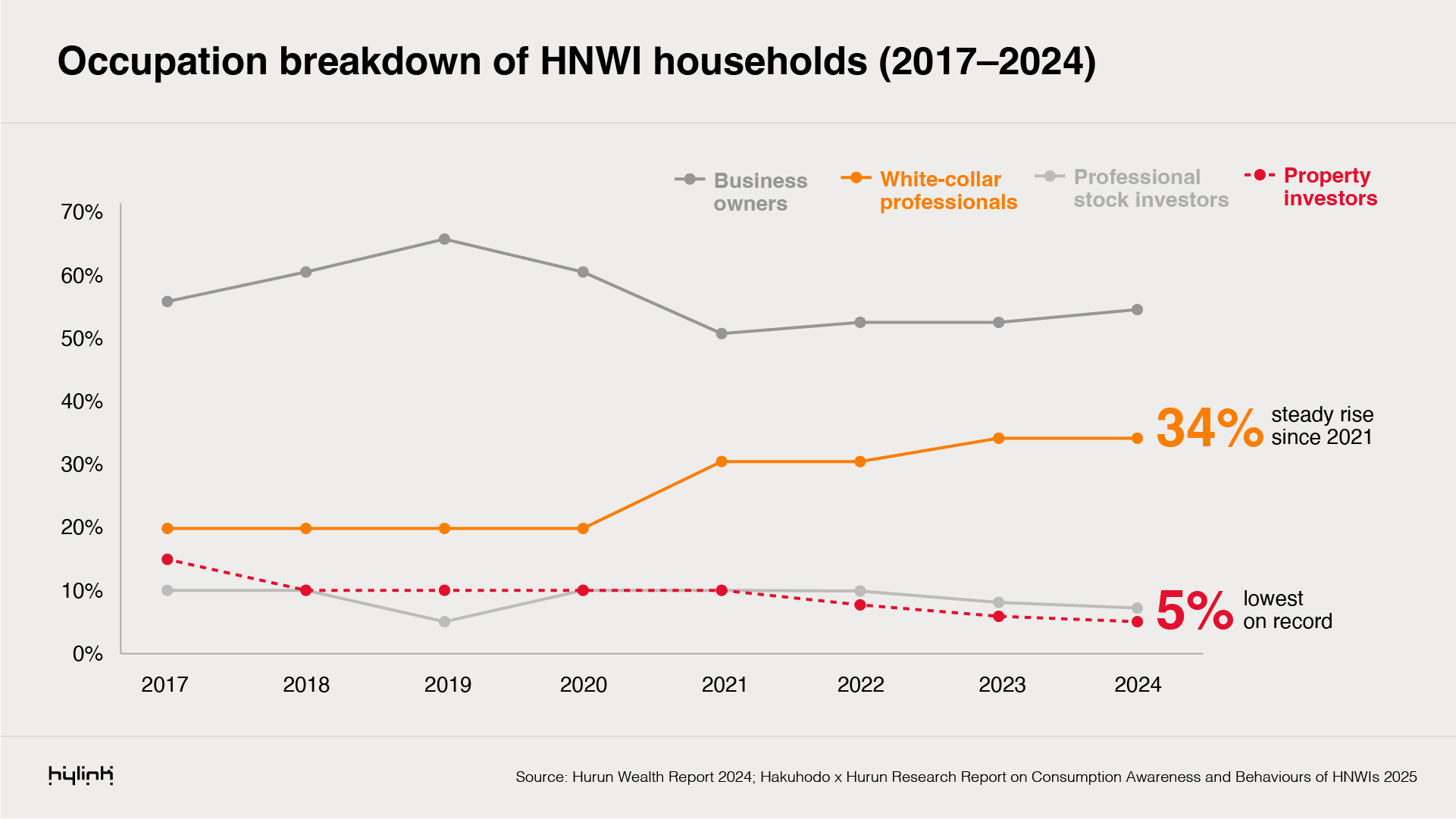

1. 2.07 million diverse households

Currently, China has approximately 2.066 million high-net-worth households (HNWIs) with net assets of RMB 10 million or above. In terms of occupation, business owners account for 54% (up 2 percentage points year-on-year), white-collar professionals 34%, professional stock investors 7%, and property investors 5%.

The share of property investors has fallen to its lowest recorded level, while the share of professional stock investors has also continued to decline. The two engines powering the growth of HNWIs over the past decade, property appreciation and equity market cycles, are losing momentum. Business acumen and professional expertise are taking their place. This structural shift towards earned wealth means brands may need to revisit strategies built around the "asset-rich" HNWI.

There is also a notable generational divide within the HNWI group. Those aged 30–44 show a stronger desire for overseas asset allocation (61% plan to increase), compared with 51% among those aged 45 and above. Conversely, the older cohort shows a stronger desire for insurance products, specifically life insurance. The 45-and-above figure is 83%, versus 75% among those aged 30–44. The same "HNWI" label covers two distinct sets of priorities, and therefore two different entry points for brands.

Source: Hakuhodo x Hurun: Research Report on Consumption Awareness and Behaviours of HNWIs 2025; YFLife x Hurun: 2025 China HNWI Financial Investment Demand & Trends White Paper

2. Health is top priority, but not in the way most think

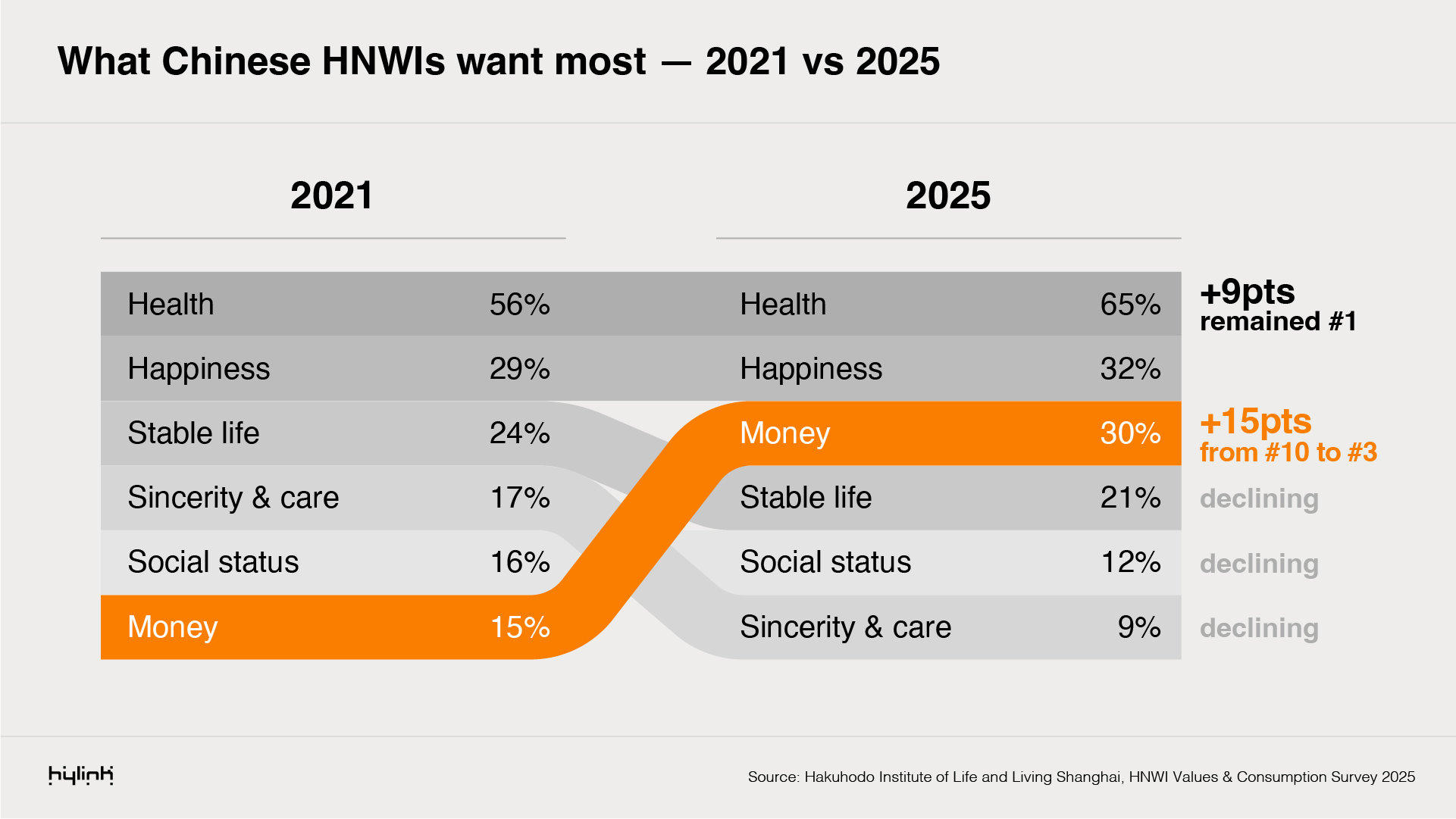

When asked to list the three most desired things in life, 65% of surveyed HNWIs named “health” as their top priority, up 9 percentage points from 56% in 2021. In the same survey, "money" jumped from 10th place to 3rd, rising 15 points over the same period.

These two simultaneous shifts may seem contradictory, but they point to the same underlying logic. In an environment of uncertainty, HNWIs tend to invest in the protection of their physical capital and reinforcement of their financial security. Both are responses to the same concern, representing a rational reallocation of resources rather than anxiety-driven behaviour.

The household data on health advisor spending is particularly revealing and varies from conventional wellness. Personal trainers (14%), nutritionists (13%), and family doctors (13%) sit alongside asset planners (13%) as the most commonly retained professionals. Physical and financial management are treated with equal priority. "Advanced health management" shows the largest gap between HNWIs and the middle class of any spending category, at +8.3 percentage points. This figure suggests that high-net-worth spending is most concentrated here.

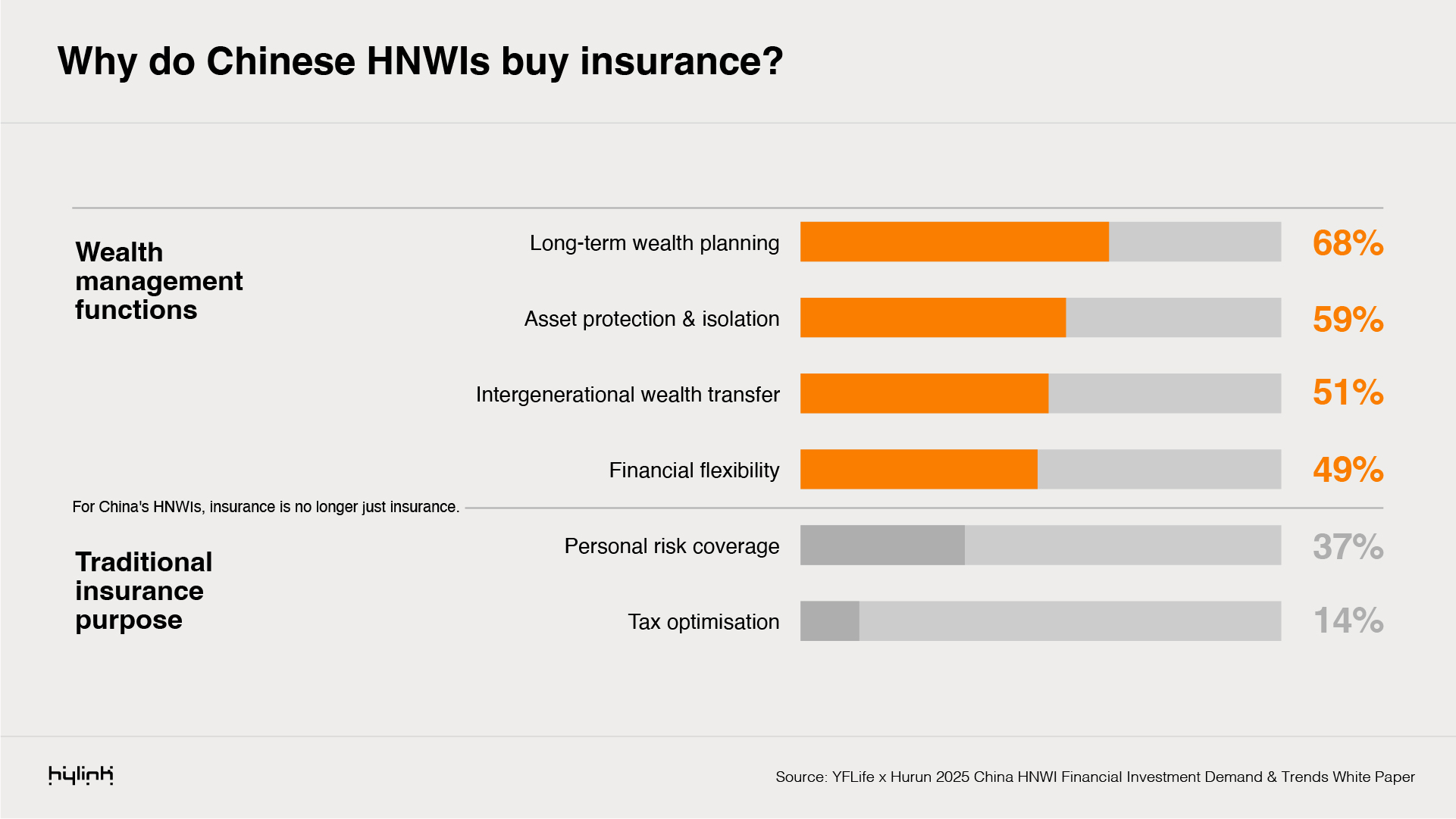

Insurance data makes the underlying logic clear. Average annual household insurance premiums among HNWIs reach up to RMB 590,000. But unlike previously, risk coverage is no longer the primary motivation. Long-term wealth planning (68%), asset protection and isolation (59%), and intergenerational wealth transfer (51%) all rank above personal risk coverage (37%). Insurance has been fundamentally redefined, now a core structural component of wealth architecture instead of a contingency plan.

Source: Hakuhodo x Hurun: Research Report on Consumption Awareness and Behaviours of HNWIs 2025; YFLife x Hurun: 2025 China HNWI Financial Investment Demand & Trends White Paper

3. HNWIs spend the most on travel, choosing based on depth of experience, not destination

Compared to other categories where HNWIs report increased spending, travel ranks first (46.8%), ahead of health and wellness (33.8%) and luxury goods (33.3%). The Hurun 2025 survey shows that HNWIs take an average of 24 holiday days per year, rising to 27 days among ultra-HNWIs (households with assets above RMB 100 million). In 2025, leisure travel grew 11%, and business travel grew 8% — among the strongest performances of any premium category.

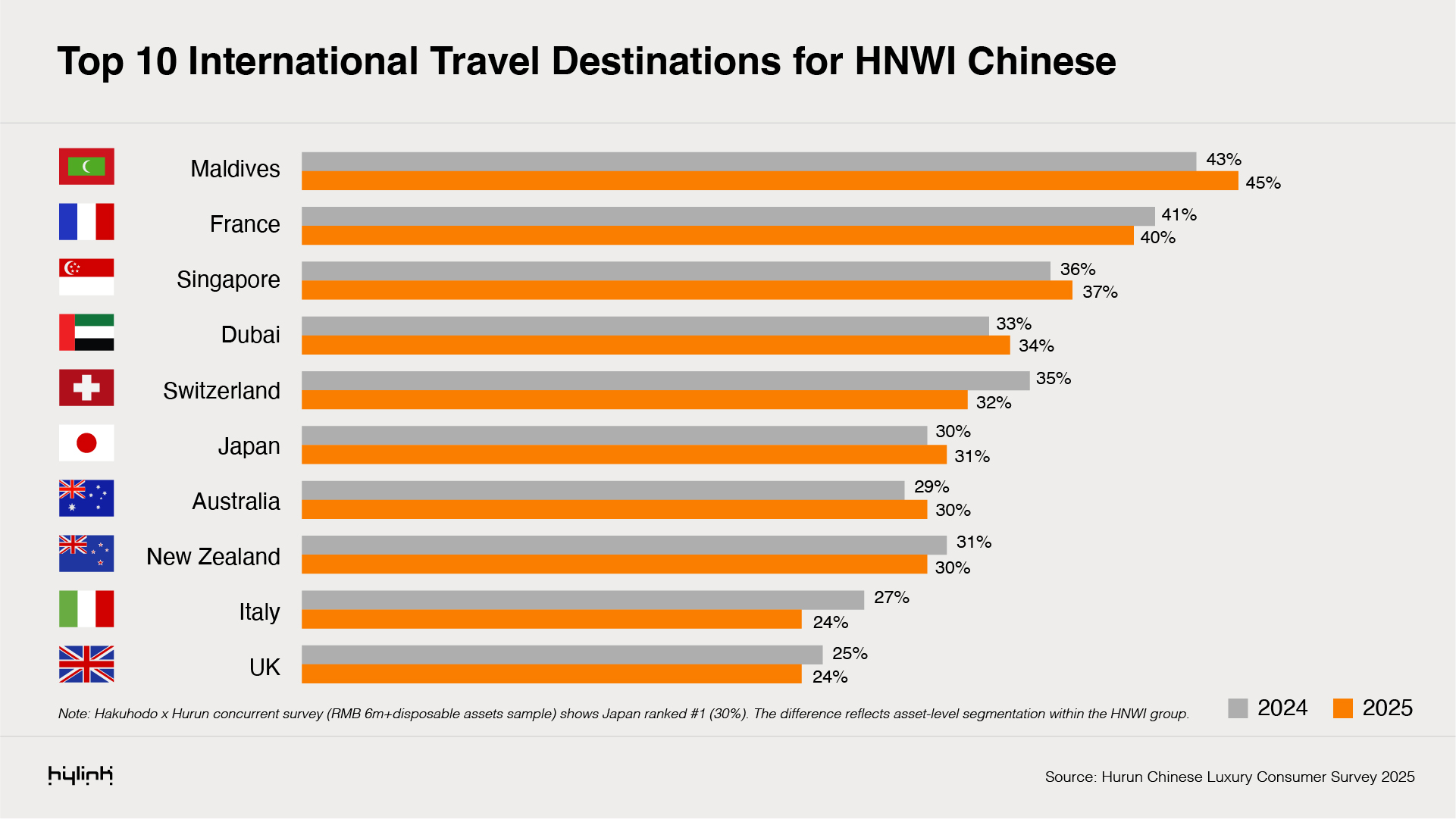

Regarding destinations, two major independent surveys produced very different rankings. In the Hakuhodo x Hurun sample, Japan emerged as the most frequently visited destination (30%) and the most-loved (29%), followed by Thailand, the US, France, and Singapore. In the Hurun luxury consumer survey, the Maldives ranked first for the fourth consecutive year (45%), with France second (40%) and Singapore third (37%).

This difference could be interpreted as a data contradiction, but we believe it’s a signal. The two surveys draw on respondents at different asset levels, with higher-net-worth individuals favouring rare destinations that inherently provide an irreplaceable experience. The broader HNWI group is more influenced by factors such as the yen exchange rate and ease of access to Japan. The global travel market is stratifying into distinct tiers, following the same logic as the luxury goods market.

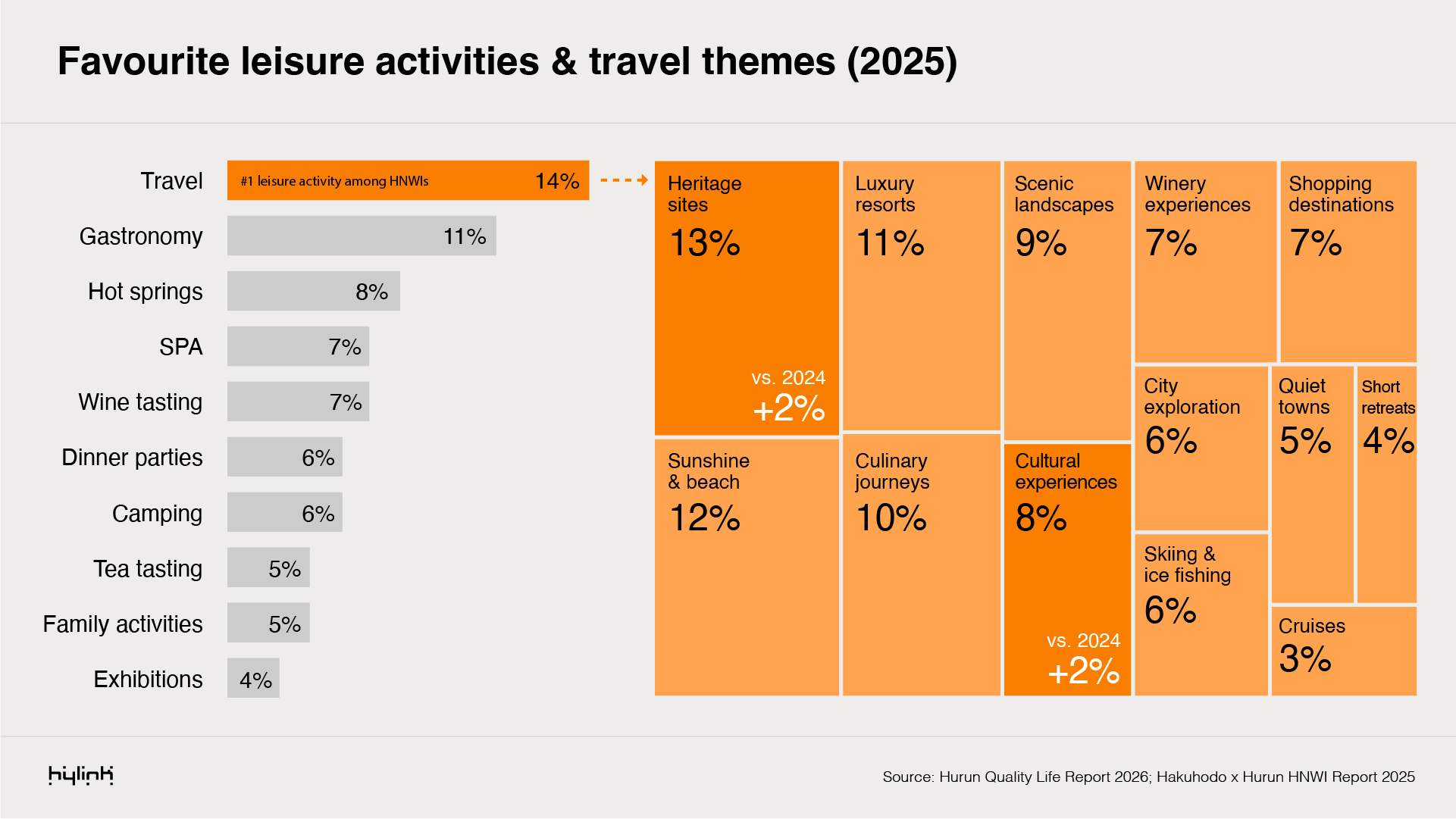

Despite these differences, both surveys agree on the categories of destinations. Heritage sites (13%) and cultural experiences (up 2 points year-on-year) have risen noticeably, sitting alongside luxury resorts (11%) as the most sought-after categories. The implication for destinations and hospitality brands is clear: the competitive advantage has shifted from the location itself to how precious the experience at the location is.

Source: Hurun Chinese Luxury Consumer Survey 2025

4. The luxury goods market is restructuring, not shrinking

The logic of luxury consumption among HNWIs is fundamentally shifting. Hakuhodo's qualitative interviews capture this directly. One respondent with assets above RMB 50 million put it this way: "Because of wealth envy, I keep a low profile day-to-day. But when I'm abroad, somewhere no one knows me, I'll wear loud colours and obvious logos." Another noted, "When something becomes accessible to most people, showing it off loses its appeal. Now I buy things with cultural value and a distinctive aesthetic." Status symbols are being upgraded, not abandoned.

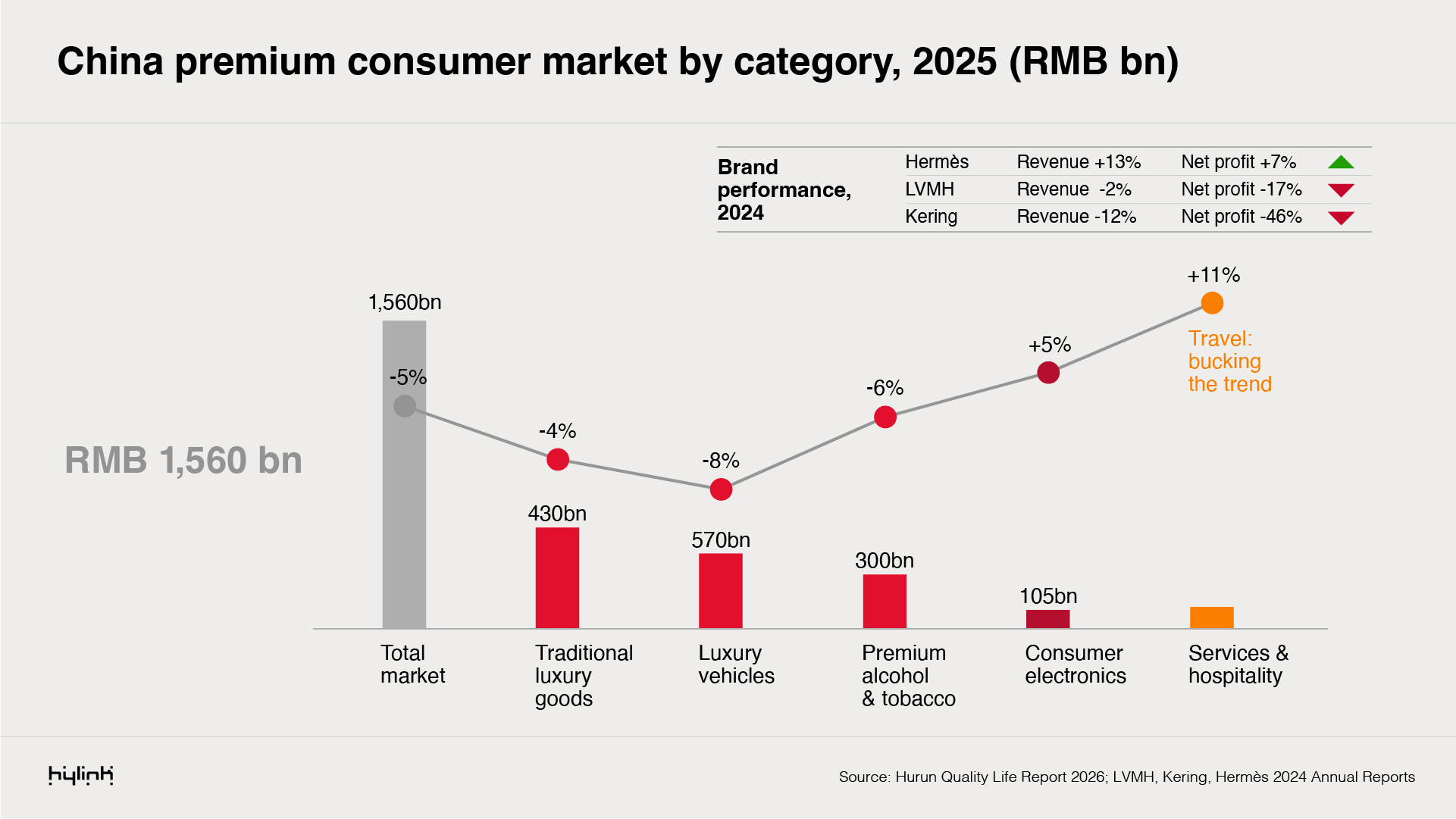

This shift in mindset directly explains the divergence visible in market data. China's premium consumer market reached RMB 1.56 trillion in 2025, down 5% year-on-year. However, category performance varies sharply: high-end watches fell 14%, high-end jewellery fell 8%, premium alcohol and tobacco fell 6%, meanwhile, leisure travel grew 11%, and business travel grew 8%. It’s important to note that demand has not completely disappeared and is being redistributed.

Brand data confirms the same pattern. LVMH reported revenue down 2% and net profit down 17% in 2024, whilst Kering saw revenue fall 12% and net profit fall 46%. Hermès grew revenue by 13% and net profit by 7%, relying on a highly scarcity-driven allocation mechanism and strict volume control. This is at the core of the brand’s competitive advantage, not due to a supply constraint. Kering's challenge is the opposite. Years of brand expansion brought its products to a wider audience, but that reach diluted the factor that drives purchase among true HNWIs — scarcity.

Source: Hakuhodo x Hurun: Research Report on Consumption Awareness and Behaviours of HNWIs 2025; Hurun Quality Life Report 2026; LVMH, Kering, Hermès 2024 annual reports

5. Overseas asset allocation is being driven by diversification, not departure

45% of surveyed HNWIs have already allocated assets to overseas financial products, with overseas holdings averaging 20% of their total portfolios. 56% say they plan to increase that allocation over the next year.

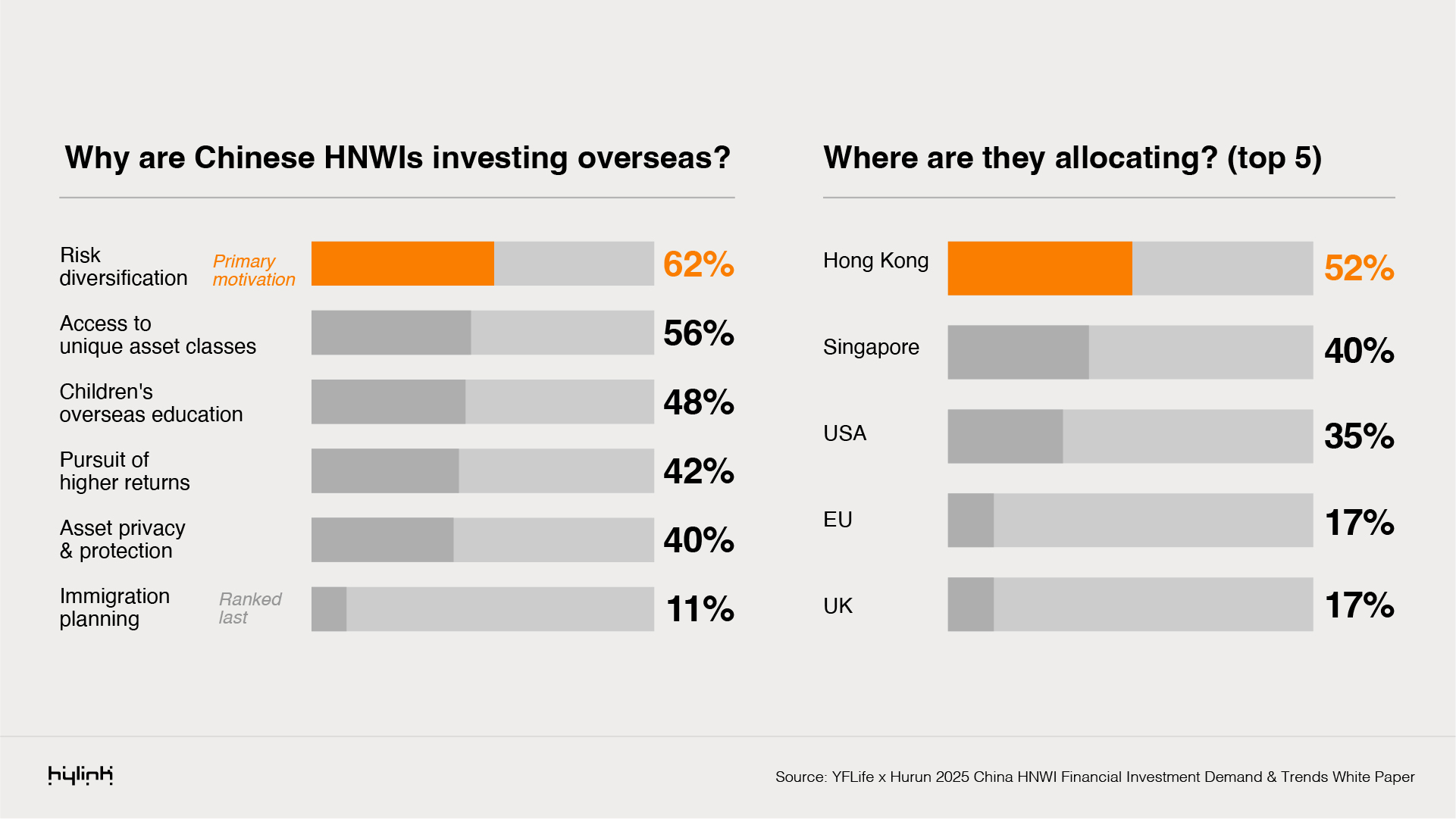

The motivations behind this trend are worth examining carefully. Risk diversification ranks first (62%), followed by access to asset classes unavailable domestically (56%), children's overseas education (48%), pursuit of higher returns (42%), asset privacy and protection (40%), and last but not least, immigration planning (11%).

That final figure is significant. A popular narrative equates rising overseas allocation with wealthy Chinese preparing to leave. However, the data tells a different story. For the majority of HNWIs, overseas investment is a natural extension of portfolio management logic, not a statement about where they want to live. The choice of destination reinforces this: Hong Kong (52%), Singapore (40%), and the US (35%) lead the rankings, all characterised by mature financial infrastructure, low correlation to RMB assets, and strong liquidity, not by immigration convenience. The Henley & Partners 2025 report puts the net outflow of Chinese HNWIs at 7,800, which is significant in absolute terms, but less than 0.4% of the 2.066 million HNWI households. The major capital movements are therefore happening at the asset allocation level, not through physical relocation.

6. The desire to spend is still there, but the bar has risen

Together, the five factors discussed above point to the same trend: the desire to spend hasn’t disappeared, but the standard for what is worth spending on has risen significantly. HNWIs are not consuming less, but simply making more deliberate choices about where they invest.

When choosing financial institutions, the factors they value most are track record and reputation (49%) and institutional capital strength (44%) — the focus is firmly on time and experience, not marketing spend. For travel destinations, recommendations shared within trusted social circles carry more weight than official promotional campaigns. For luxury goods, recognition within their own peer group matters more than large-scale brand campaigns. To cross their minds, brands must run through the channels that HNWIs already trust.

Their expectations of service providers have also evolved. When asked what they most desire from insurance companies, the top responses were retirement planning (56%), education fund planning (55%), and wealth transfer services (53%). None of these are traditional financial products, but actually life planning services. Providers who engage with this desire will benefit from a fundamentally closer relationship than those who focus on selling products alone — and this gap is widening. The same logic applies to every brand and destination that wants to reach this group.

Source: YFLife x Hurun: 2025 China HNWI Financial Investment Demand & Trends White Paper

Closing thoughts

The growth logic that relied on brand expansion and broad market reach is losing traction with true HNWIs. For this group, mass appeal is a drawback, not a selling point.

China's genuine high-net-worth consumers are increasing their health spending, travel budgets, desire for rare products and experiences, insurance cover, and overseas asset allocation. That growth is flowing to brands and institutions that offer irreplaceable experiences, build genuine trust, and respond to what this group actually needs.

The market has not shrunk. The direction of spending has changed.

Sources

YFLife x Hurun: 2025 China HNWI Financial Investment Demand & Trends White Paper (Aug–Sep 2025, n=500, quantitative survey)

Hakuhodo x Hurun: Research Report on Consumption Awareness and Behaviours of High-Net-Worth Individuals 2025 (published 27 June 2025)

Hurun Quality Life Report 2026 (published January 2026)

Hurun Chinese Luxury Consumer Survey 2025 (via Dragon Trail): https://www.dragontrail.com/resources/blog/hurun-chinese-luxury-consumer-survey-2025

Henley Private Wealth Migration Report 2025: https://www.henleyglobal.com/newsroom/press-releases/henley-private-wealth-migration-report-2025

Bain & Company China Personal Luxury Report 2025: https://www.bain.com/about/media-center/press-releases/2026/chinas-personal-luxury-market-contracts-35-in-2025-but-shows-signs-of-recovery/